Have rising interest rates dampened enthusiasm for collector cars?

Car collectors overwhelmingly own their cars outright, but borrowing money to acquire a dream car is more common than you might think. As you would expect, macro financing trends do have implications for the collector car market, and with rising interest rates, a corresponding decrease in vehicles financed would be expected. It turns out, though, that while some segments of the collector car market are evolving as a result of changes in lending rates, the bigger picture is largely unchanged. Let’s dig in.

When we looked at financing trends a year ago, a small but significant portion of collector cars—3.8 percent—were financed. Interest rates have increased by three points over the last 12 months, so surely the share of financed collector cars decreased, right? No. In fact, it’s ticked up ever so slightly to 3.9 percent. What has changed is more subtle.

The amount of financing we see for newer performance vehicles in particular is tied to the returning signs of depreciation for those vehicles that we noted recently. With lenders tightening standards and interest rates up quite a bit, premiums for the latest and greatest vehicles are shrinking.

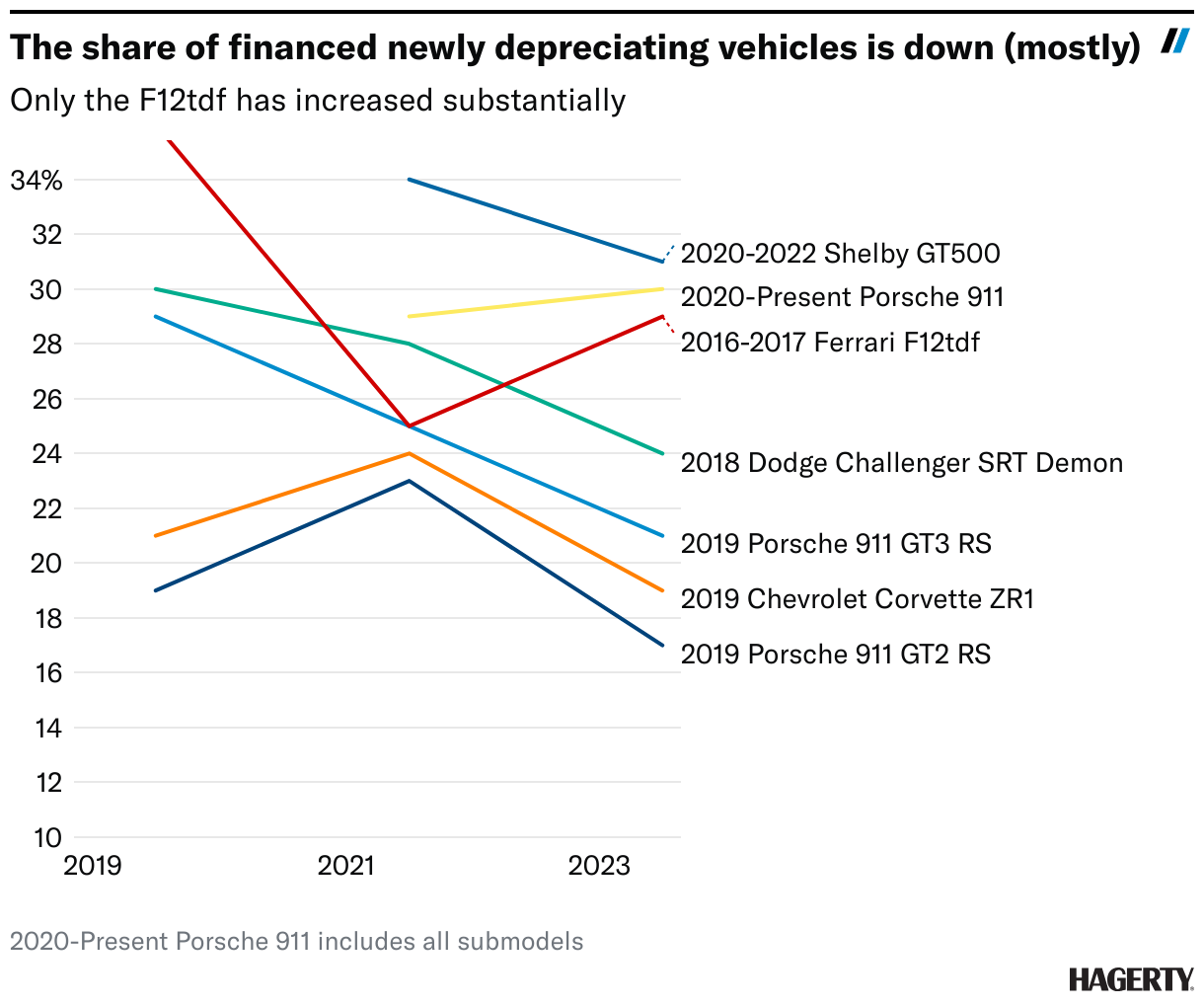

How likely is it that modern collector vehicles, like C7 Corvette ZR1s and 911 GT3s, are financed? Our policy data shows that 30 percent of 2020+ Porsche 911s (992 generation) are financed, which is up one percent from 2021. However, many other vehicles that are beginning to depreciate again have a shrinking share financed. Only the Ferrari F12tdf, the values of which just recently ticked slightly downward from a hot streak, has a growing share.

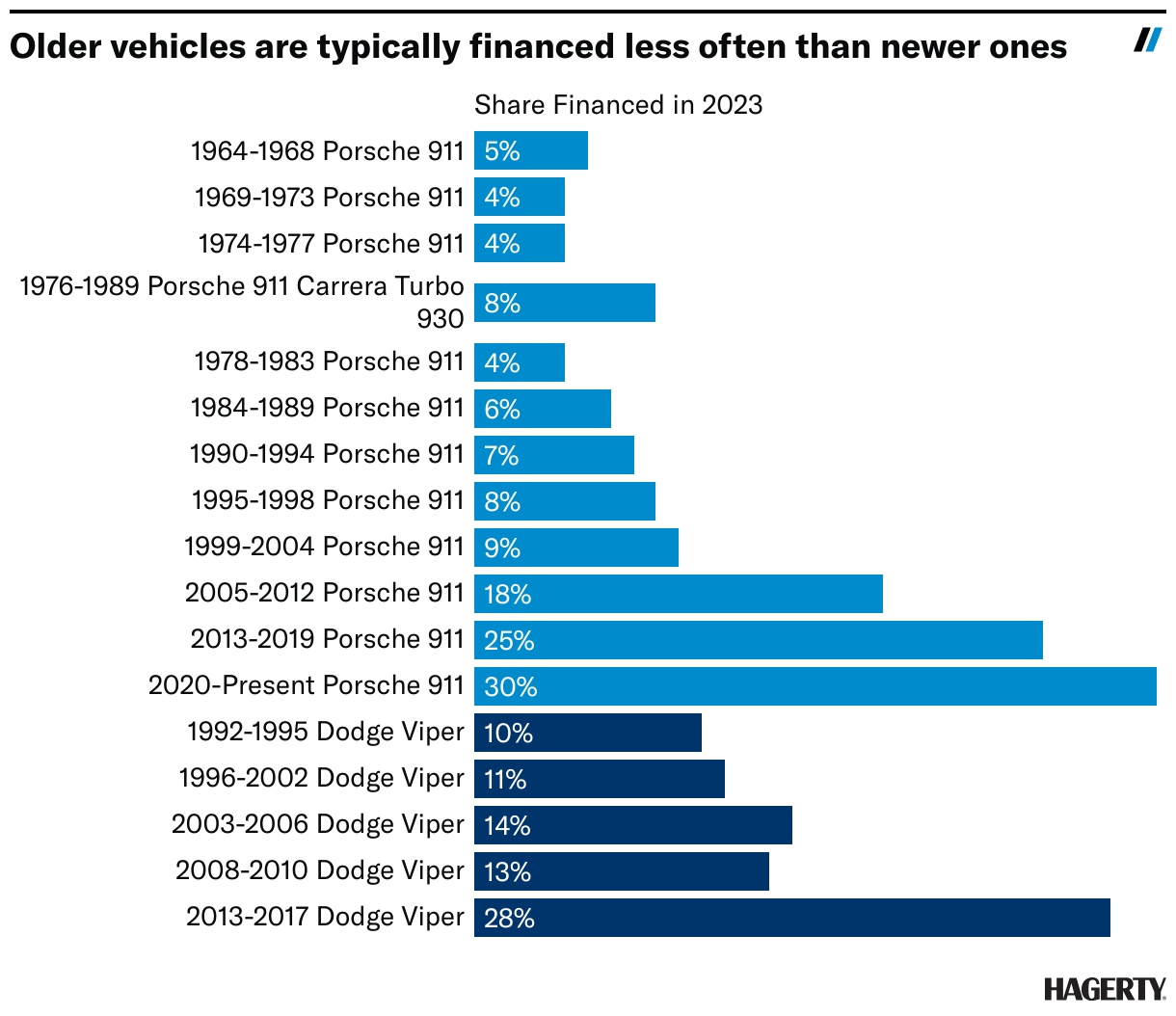

Another vehicle that’s regularly financed is the 2006–15 Bugatti Veyron. Presently, 29 percent of Veyrons insured by Hagerty are financed, up from 13 percent in 2019, but down from last year’s high of 40 percent. The Veyron’s high proportion appears to be an aberration, however—historically, as vehicles increase in age, they’re less likely to be financed, and that remains the case. The Porsche 911 and Dodge Viper, for example, demonstrate this well:

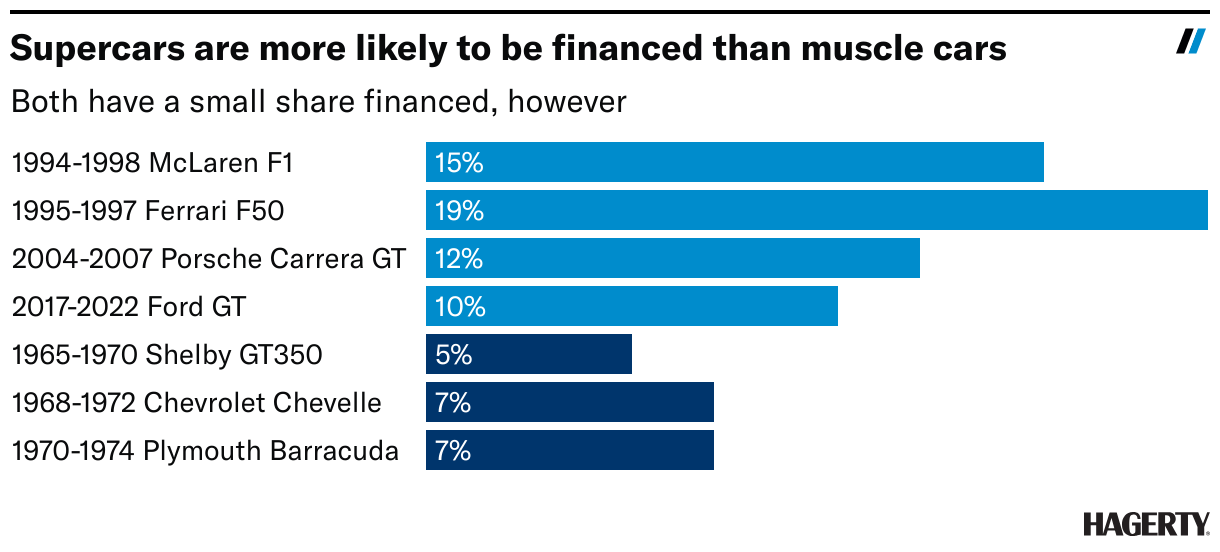

Aside from the Veyron, supercars like the Ferrari F50, McLaren F1, Porsche Carrera GT, and 2017– Ford GT have a small and decreasing share of vehicles financed. Meanwhile, many popular muscle cars show an even smaller share of vehicles financed. The original Shelby GT350, Plymouth ‘Cuda, and Chevrolet Chevelle are all in the single digits.

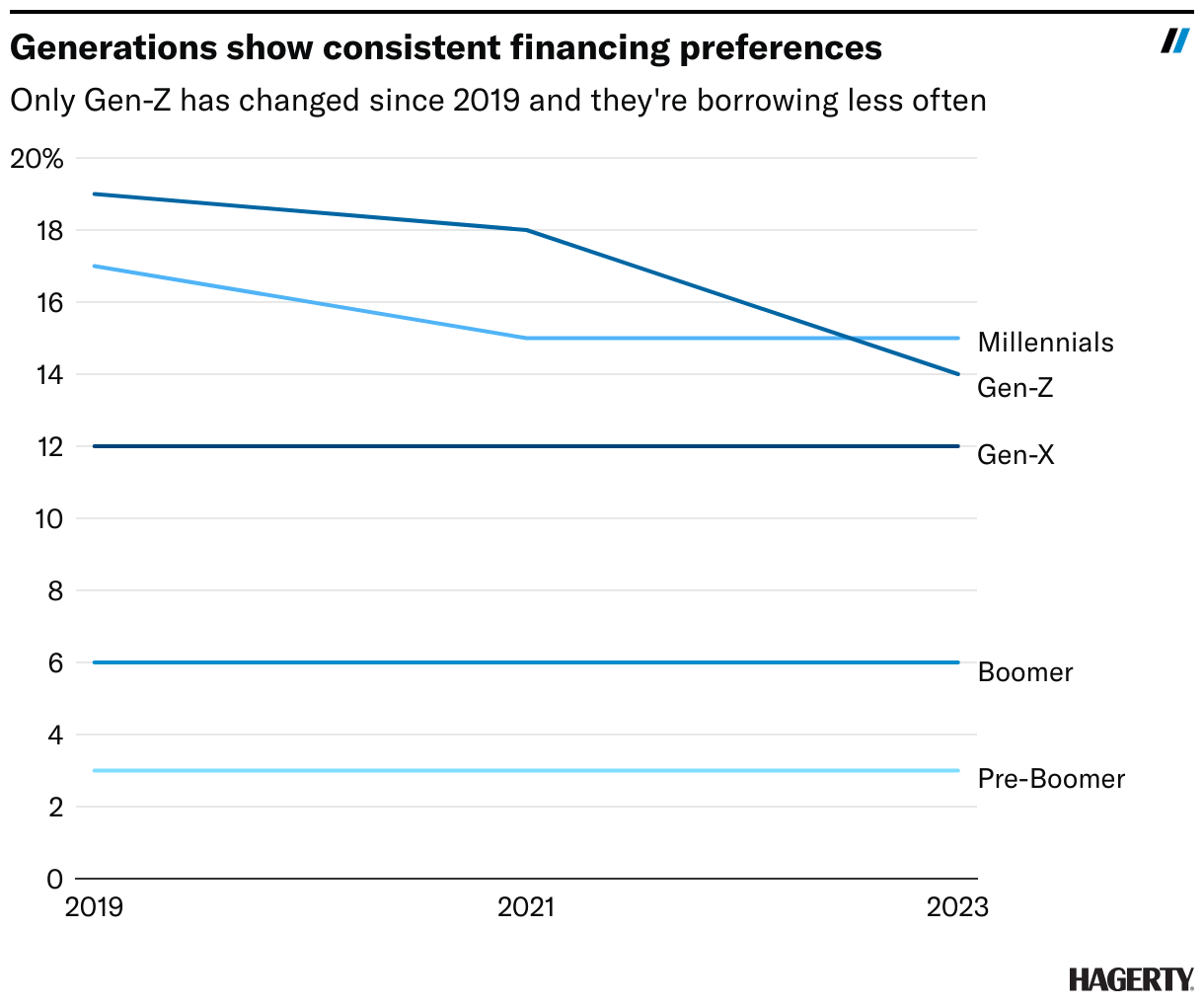

When it comes to owner demographics, younger generations are more likely to finance a vehicle than older generations. Each cohort’s share has been consistent since 2019, except for the youngest (Gen Z, 1997–2010). That said, their move away from financing may be due to their vehicle preferences and tightening lending standards.

The collectors more likely to use financing also tend to own fewer vehicles. Typically, they have about half as many vehicles compared to those that do not use financing. Similarly, the total collection value among borrowers is less than half that of those not financing.

The upshot is that yes, we are seeing some movement at the points traditionally and statistically most likely to be impacted by changes in access to capital. But the fact that the overall percentage of collector vehicles has inched upward despite a three-point increase in rates suggests a noteworthy (and stabilizing) resilience, perhaps driven by a willingness to make a luxury purchase regardless of rate, or because in some cases buyers are benefitting from the rates through other investments.

***

Check out the Hagerty Media homepage so you don’t miss a single story, or better yet, bookmark it. To get our best stories delivered right to your inbox, subscribe to our newsletters.

Depends on the car and how it is financed.

Also a big player is the stock market. If it is a bull and running wild people keep their money in their investment’s. If the market is dropping and weak people pull their money and buy cars and other things.

Now if the market goes on a good run after Biden is gone I see many cars being sold and the money going back into the marker.

I bought my latest car with investment money as my stocks took a big hit since the last election. To stem the loss and retain value I bought a car I like.

This is nor for every car and every investor. With what I paid and if I should sell it I should come out even to ahead.

Not sure how much this varies by state (or province).

Where I live good luck getting any reasonable sort of loan to finance anything over 6 years old. You can get the high interest ’cause you are high risk loans for the 9 year old used cars from some sketchy dealerships but it isn’t a deal that make sense outside of no choice.

The current dealer finance rates for any used are punishing for those of us used to 0-1.4% kind of deals.

A straight-up loan to buy a collector car? I don’t see that around here, but I don’t swim in the vintage Ferrari world either. Your workaround here (not saying this is wise) is to get a line of credit (which around here are all home-equity based it seems) and buy the car with that. This is better (in most cases) than buying your collector car on a credit card but not by much.

Few buy Ferraris on loans like this. But it does hurt the Camaro and Mustang crowd.